Helping Vancouver Island folks get the mortgage they deserve since 2008

I have been helping Comox Valley families get mortgages since 2008. My team specializes in the situations that take real expertise: self-employed, bank declined, debt consolidation, and reverse mortgages. We live here, we know this market, and we pick up the phone.

Where We Shine

The files that take more than

a standard application.

Not every mortgage situation is straightforward. If yours is not, that is exactly where we are most useful. Eighteen years on the Island means we have seen it all.

VICTOR ANASIMIV

Mortgage Broker — Comox Valley, BC

I have been helping people in the Comox Valley get mortgages since 2008. In that time I have learned that what clients actually want is pretty simple: someone who is honest with them, explains things clearly, and handles the complicated parts so they do not have to.

That is what I try to do every single time.

I live here. I have bought property here. I know this market from both sides of the transaction, and I understand that buying a home or refinancing a mortgage is one of the biggest financial decisions most people will ever make. It should not feel overwhelming. It should feel like you have someone in your corner who knows what they are doing and genuinely cares how it turns out for you.

Through Modern Mortgage Group and Dominion Lending Centres, I have access to a wide network of lenders, including major banks, credit unions, and specialty trust companies, which means I can find options that fit your specific situation rather than fitting you into whatever one institution happens to offer. My clients span the length of Vancouver Island, across BC and all over Canada.

Here is what working with me actually looks like:

I find mortgage options that fit your financial goals, not just the ones that are easiest to approve. I explain what everything means in plain language, no fine print surprises. I manage the entire application process from start to close so you are not chasing down documents or wondering what is happening. And I am available when you have questions, which in my experience is exactly when most people need their broker the most.

You have a lot going on. Let me handle the mortgage.

The Team

More Licensed brokers

working on your file.

When you work with us you are not waiting on one person. You have a full team of licensed professionals behind your mortgage from start to finish.

How It Works

Simple process, no surprises.

Good Questions

Things people usually want to know.

How do I get started?

Just reach out. Call 250-338-3740, send an email, or fill out the contact form. We will have a conversation about your situation, tell you what your options look like, and go from there. No paperwork required to have that first conversation.

My bank said no. Is that the end of the road?

Not even close. Banks decline a lot of files that are perfectly approvable at the right lender. We work with a range of alternative lenders who handle these situations every day. Tell us what happened and we will give you an honest read on what is possible.

I run my own business. Will that make it harder to qualify?

It depends on how your income is documented, but it is rarely as complicated as people expect. The trick is finding the right lender for your specific income structure. We have arranged a lot of self-employed mortgages on Vancouver Island and we know which lenders look at these most fairly.

What is a reverse mortgage and is it right for me?

A reverse mortgage lets homeowners 55 and older access the equity they have built up without making monthly payments. It is not right for everyone, but for some people it is genuinely life-changing. We walk you through everything clearly, including the parts that do not always get mentioned, so you can make a real decision.

What does it cost to work with you?

In most cases nothing. The lender pays our fee when your mortgage closes. For private or alternative lending situations there are sometimes fees, and we always explain those clearly upfront before going any further.

How long does mortgage approval take in BC?

A pre-approval can typically be completed within 24–72 hours. Full mortgage approval after an accepted offer usually takes 5–10 business days depending on the lender and the complexity of your file. I manage the entire process and keep you updated at every stage — you'll never be left wondering where things stand or chasing me for an update.

What is B-lending and who does it help?

B lenders are alternative institutional lenders whose entire purpose is to approve files that major banks decline. They accept lower credit scores, alternative income documentation, and non-standard situations. Their rates are typically a bit higher than a bank, and they usually require 20% down. For many clients they are the bridge that gets them into a property and then transitions to conventional lending at renewal once their situation has improved.

Can you help someone with credit challenges?

Yes. A past credit issue does not automatically mean no mortgage. What matters is the full picture: what caused the problem, how long ago it was, and what your situation looks like now. We review the credit history carefully before recommending any lender so you are not wasting hard inquiries on applications that are unlikely to succeed.

What is debt consolidation through a mortgage and when does it make sense?

If you own a home in the Comox Valley and have built meaningful equity, you can refinance your mortgage to access that equity and use it to pay off high-interest consumer debt. The result is replacing multiple high-rate payments with a single lower-rate one. The math is often compelling. We run the numbers honestly and only recommend it when it genuinely makes sense for your specific situation.

How does mortgage renewal work and should I just sign my lender's offer?

Your mortgage renewal happens at the end of each term. Your lender sends a renewal offer, but that offer is almost never their best rate. It is a starting position designed to capture clients who do not shop around. We compare the full market before your maturity date and tell you honestly whether staying with your current lender or switching makes more financial sense. There is no penalty for switching at maturity.

Do you only help people in the Comox Valley?

No. We help clients across all of Vancouver Island, throughout BC, and across Canada. Courtenay is home base but the mortgage process works just as well over the phone or a video call. If you are anywhere on the Island, please reach out.

What areas of Vancouver Island do you serve?

All of it. We work with clients in Nanaimo, Victoria, Campbell River, Parksville, Qualicum Beach, Port Alberni, Duncan, Lake Cowichan, and everywhere in between. We also serve clients throughout the rest of BC and across Canada. Distance is not a barrier for us.

Still have a question?

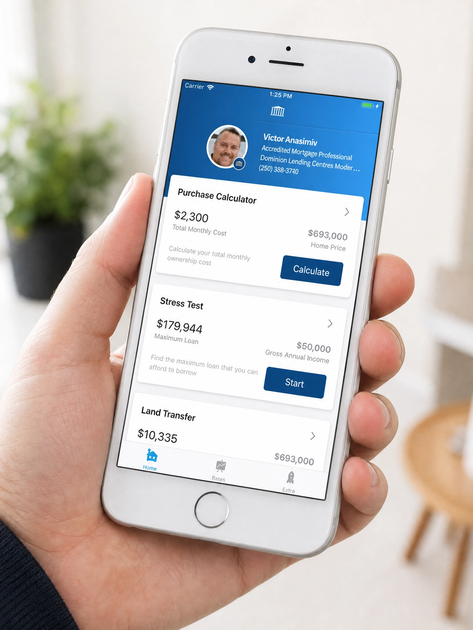

My Mortgage App

Manage your mortgage from your phone.

Download my app to access mortgage calculators, track your application, securely upload documents, and stay connected with me throughout the process — all in one place.

Our Lender Network

I've developed excellent relationships with many lenders across the country.

Let's figure out which one has the best product for you.

Our Sponsors

Real mortgage advice for real life on Vancouver Island.